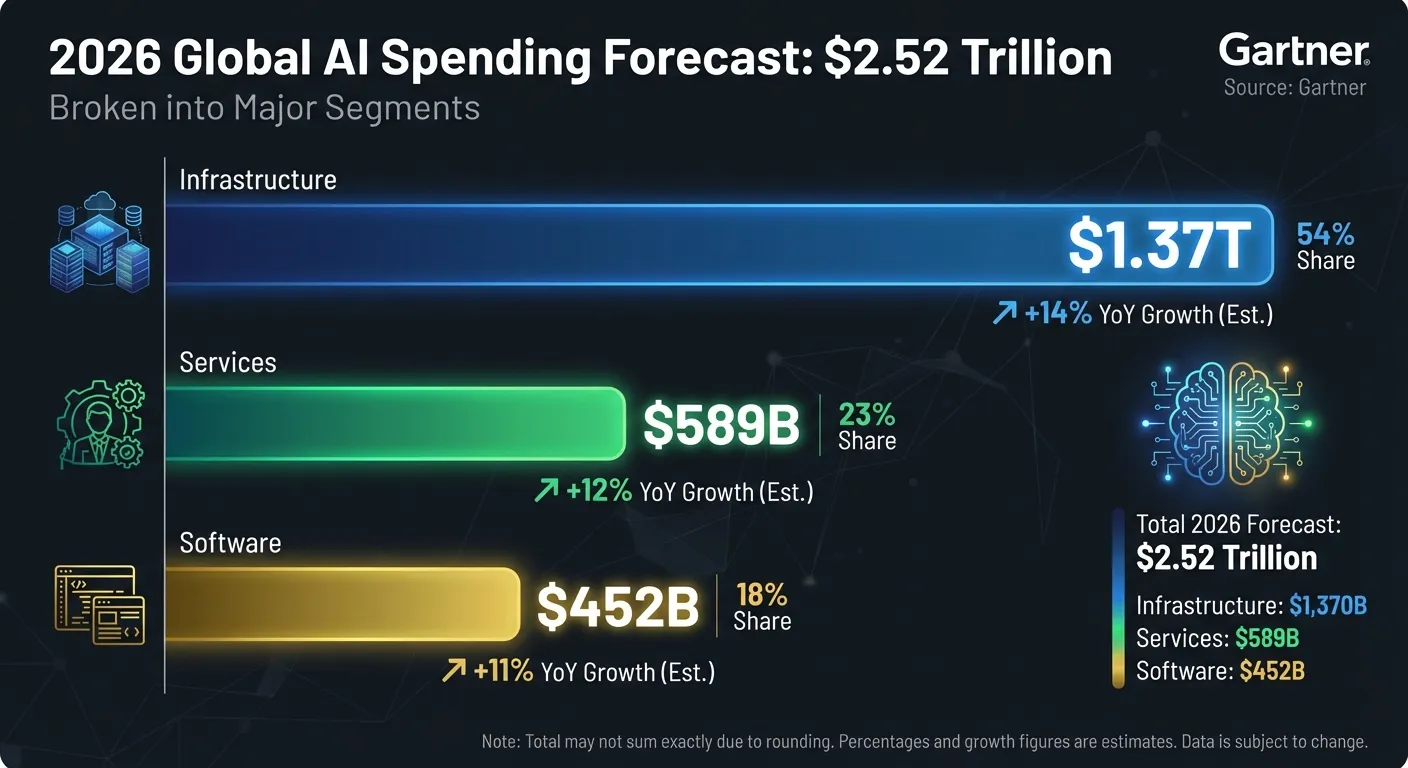

Two and a half trillion dollars. That's what the world will spend on artificial intelligence in 2026, according to Gartner's latest forecast released in mid-January. The $2.52 trillion figure represents a 44% jump from the $1.76 trillion spent in 2025, a growth rate that would be jaw-dropping in any industry but feels almost routine in an AI sector that has shattered spending records year after year. To put the number in perspective: the entire GDP of France was roughly $3.1 trillion in 2025. The AI industry alone is approaching that scale.

But the most revealing story isn't the top-line number. It's where the money is actually going, and what that distribution says about whether this spending spree is building something durable or inflating a bubble that even Gartner acknowledges is in the "Trough of Disillusionment."

The infrastructure-heavy spending pattern suggests an industry still laying foundations rather than harvesting returns. That's not necessarily a bad thing, the internet looked the same in the late 1990s before generating trillions in economic value. But it means the hardest question in technology right now isn't "Can AI do amazing things?" It's "When do companies start seeing returns proportional to what they're investing?"

Following the Money: Infrastructure Eats Everything

AI infrastructure will account for $1.37 trillion of the total spend, up from $965 billion in 2025. That's a 42% increase, driven primarily by investments in AI-optimized servers, which alone will surge 49% year-over-year. Server spending represents 17% of total AI expenditure, reflecting the simple physical reality that training and running AI models requires massive amounts of specialized computing hardware.

The infrastructure category includes more than just servers. Data centers are being built at an unprecedented pace, with companies like Microsoft, Google, Amazon, and Meta each committing tens of billions to new facilities. The actual construction of AI-related infrastructure will add $401 billion in spending in 2026, money flowing to real estate developers, construction firms, electrical utilities, and semiconductor manufacturers.

John-David Lovelock, Distinguished VP Analyst at Gartner, noted that "AI infrastructure growth remains rapid despite concerns about an AI bubble, with spending rising across AI-related hardware and software." The statement carries a deliberate acknowledgment of bubble fears while affirming that the spending trend continues regardless. It's the kind of careful positioning that reflects how analysts are navigating the tension between documenting genuine transformation and maintaining credibility if the music stops.

Nvidia remains the primary beneficiary of infrastructure spending. The company's GPUs power the vast majority of AI training and inference workloads, and demand has consistently outstripped supply. But competitors are emerging. AMD, Intel, and custom silicon from Google (TPU) and Amazon (Trainium and Inferentia) are capturing growing shares of the market. OpenAI's recent partnership with Cerebras signals that the chip supply chain is diversifying, which should eventually moderate infrastructure costs.

Software and Services: The Growth That Matters More

While infrastructure dominates the raw numbers, the software and services segments tell a more nuanced story about where AI is actually being used. AI software spending is projected to reach $452 billion in 2026, up from $283 billion in 2025, a 60% increase that reflects growing enterprise adoption of AI-powered tools. Generative AI model spending specifically is growing at 80.8%, with GenAI's share of the overall software market rising by 1.8 percentage points.

AI services, including consulting, implementation, and managed services, will reach $589 billion, up from $439 billion. This growth indicates that enterprises are moving beyond experimentation into production deployments that require professional support. Companies are hiring consultants to build AI strategies, systems integrators to deploy solutions, and managed service providers to keep everything running.

The services growth is particularly significant because it signals the maturation of the AI market. During the hype phase, companies bought AI tools and experimented. During the current phase, they're investing in the human expertise needed to make those tools productive. Consulting firms like McKinsey, Accenture, and Deloitte have all expanded their AI practices dramatically, hiring thousands of specialists to meet enterprise demand.

The software segment's trajectory matters because it reflects actual product adoption rather than speculative investment. When a company buys an AI-powered CRM tool or deploys a coding assistant like GPT-5.3-Codex, that spending directly correlates with work being done. Infrastructure spending, by contrast, is a bet on future demand that may or may not materialize at the scale investors hope.

The "Trough of Disillusionment" Problem

Gartner's own hype cycle framework places AI squarely in the "Trough of Disillusionment" for 2026, the phase that follows peak hype and precedes the "Plateau of Productivity" where technology delivers sustained, realistic value. This positioning shapes how the spending numbers should be interpreted.

Lovelock was explicit about the implications: "Because AI is in the Trough of Disillusionment throughout 2026, it will most often be sold to enterprises by their incumbent software provider rather than bought as part of a new moonshot project." In other words, enterprises are becoming more conservative about AI spending, preferring to add AI capabilities to existing vendor relationships rather than launching ambitious new initiatives.

He added a crucial caveat: "The improved predictability of ROI must occur before AI can truly be scaled up by the enterprise." This is the gap between spending and value that haunts the AI industry. Companies are investing $2.52 trillion collectively, but many individual organizations struggle to demonstrate that their AI investments generate positive returns.

The ROI challenge varies dramatically by use case. Customer service chatbots, code generation tools, and data analysis applications have shown clear productivity gains. More ambitious projects, autonomous agents managing complex workflows, AI replacing entire business processes, remain unproven at scale. The gap between what AI can do in demos and what it delivers in production environments continues to frustrate CIOs who need to justify budgets to their boards.

Winners, Losers, and the Concentration Question

The $2.52 trillion isn't distributed evenly. A handful of companies capture the majority of AI spending. Nvidia's data center revenue alone was projected to exceed $100 billion in 2025, with 2026 expected to be even larger. Microsoft, Google, Amazon, and Meta collectively spend hundreds of billions on AI infrastructure. OpenAI, Anthropic, and a small cluster of AI labs consume a disproportionate share of compute resources.

This concentration raises questions about market health. When a small number of companies both drive and capture AI spending, the ecosystem's resilience depends on those companies maintaining their momentum. An Nvidia supply disruption, a major cloud provider outage, or a shift in enterprise sentiment could ripple through the entire $2.52 trillion market.

The geographic distribution also matters. The United States captures the lion's share of AI spending, with China, the European Union, and others competing for smaller but growing portions. US export controls on advanced AI chips have created a bifurcated market where American and allied companies develop one set of capabilities while Chinese firms like DeepSeek pursue different approaches, sometimes achieving comparable results at lower cost.

For smaller companies and startups, the spending explosion creates both opportunity and challenge. Opportunity because enterprise demand for AI solutions is enormous and growing. Challenge because competing with mega-cap technology companies for talent, compute resources, and customer attention requires either significant funding or a clearly differentiated product.

What These Numbers Actually Mean

The $2.52 trillion figure is both impressive and incomplete. It tells you that the AI industry is massive and growing rapidly. It doesn't tell you whether that growth will generate proportional economic value or whether the current spending rate is sustainable. History offers cautionary parallels: the dot-com boom saw similar explosive investment before a painful correction, even though the underlying technology eventually delivered on its promise and then some.

The most encouraging signal in Gartner's data is the growth in services and software spending relative to infrastructure. As these segments grow, it suggests that AI is moving from the "build the foundations" phase into the "use the tools" phase. The most concerning signal is that infrastructure still dominates, indicating that the foundations are still being laid rather than being fully utilized.

For business leaders making AI investment decisions in 2026, the Gartner data provides context but not answers. The spending is real, the growth is undeniable, and the competitive pressure to invest is intense. Whether individual companies see returns depends on execution, use-case selection, and realistic expectations about what AI can deliver today versus what it might deliver in the future.

Sources

- Gartner Says Worldwide AI Spending Will Total $2.5 Trillion in 2026 - Gartner

- Gartner: Global AI spending to reach $2.5 trillion in 2026 - Computerworld

- AI spend to reach US$2.5T but ROI remains elusive, says Gartner - ARN

- Gartner Forecasts Worldwide IT Spending to Grow 10.8% in 2026 - Gartner

- Enterprise tech spending to cross $6 trillion in 2026, driven by AI infrastructure boom - Computerworld