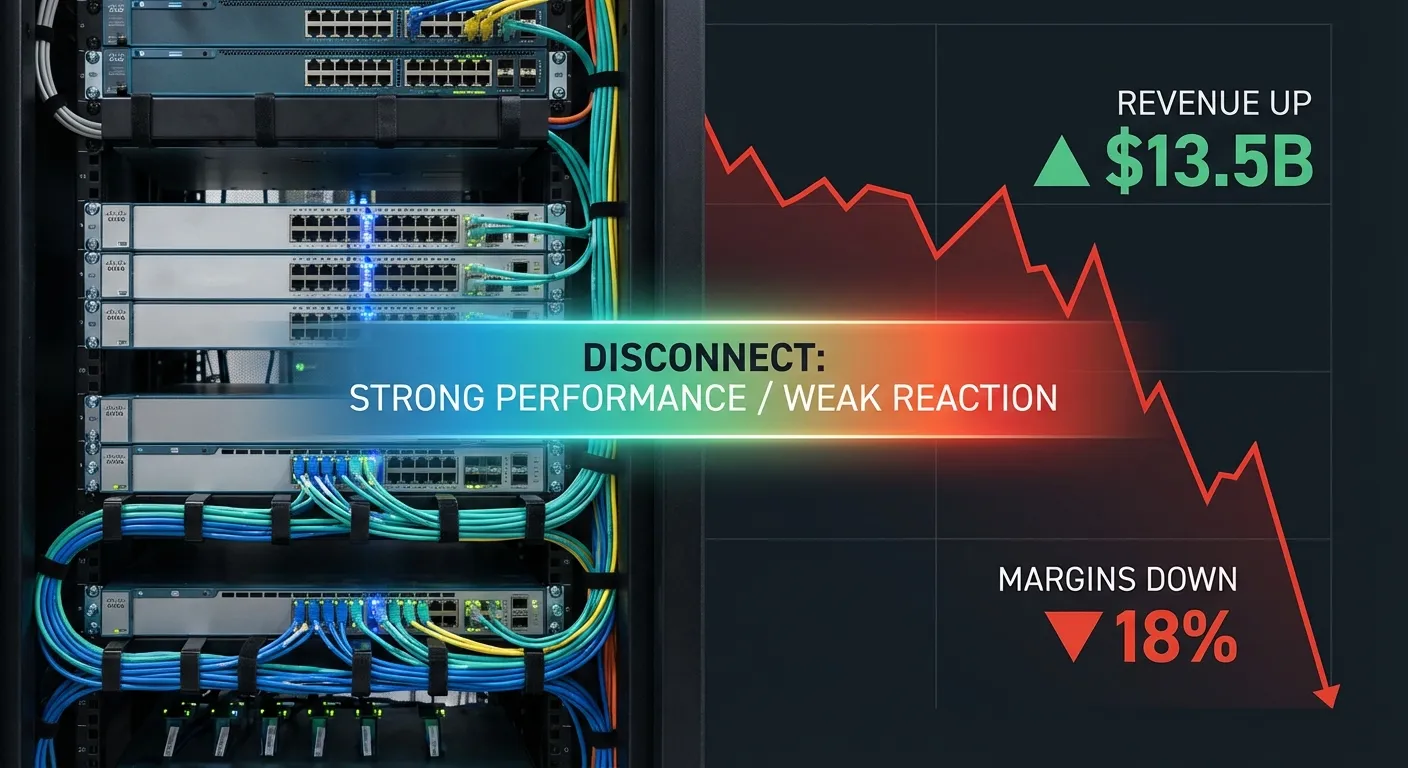

Cisco did almost everything right in the second quarter. Revenue came in at $15.3 billion, beating Wall Street's estimate of $15.11 billion. Earnings per share hit $1.04, above the $1.02 consensus. Networking revenue surged 21% year-over-year to $8.29 billion. The company even launched a new AI chip, the Silicon One G300, and projected AI-related orders would exceed $5 billion this fiscal year.

And the stock dropped 5% after hours on Wednesday, with some analysts projecting a steeper decline in Thursday's regular session.

The culprit wasn't what Cisco earned. It was what Cisco is paying for the components that make its products, specifically the memory chips that have become the most contested commodity in the tech supply chain. Cisco's quarterly gross margin came in at 67.5%, below the 68.14% analysts expected. And its full-year revenue outlook of $61.2 to $61.7 billion missed the $63.9 billion Wall Street was banking on by more than $2 billion.

In a market obsessed with AI profitability, even a fraction-of-a-percent margin miss can wipe out billions in market value. Cisco just learned that lesson in real time.

The Memory Chip Problem Nobody Saw Coming

The story behind Cisco's margin squeeze has less to do with Cisco and more to do with the insatiable appetite of AI infrastructure buildouts that are reshaping global supply chains.

OpenAI, Google, Microsoft, Amazon, and Meta are collectively pouring hundreds of billions of dollars into data centers to support their AI ambitions. That spending, which Gartner recently forecast would reach $2.52 trillion globally this year, has created enormous demand for high-bandwidth memory chips, the kind that go into AI accelerators, networking switches, and the optical equipment that connects it all. Memory chip manufacturers have responded rationally: they're prioritizing production of higher-margin data center components over everything else.

The result is that companies like Cisco, which need memory chips for their networking equipment but can't match the per-unit margins that AI accelerator makers command, are paying more for the same components. It's a supply chain squeeze that hits profitability even when demand for the end products is strong. Cisco CEO Chuck Robbins acknowledged the pressure directly, telling analysts that management "has raised prices and is reworking customer contracts" to offset the higher input costs.

Barclays analysts noted the margin weakness was unexpected, pointing to a shift in Cisco's product mix toward optical and AI switch products that carry different cost structures than traditional networking gear. In other words, the very products driving Cisco's revenue growth are also the ones most exposed to memory chip price inflation. Growth and margin pressure are coming from the same source.

The Disconnect Between Revenue and Reaction

To understand why Wall Street punished Cisco despite strong top-line numbers, you have to understand how the market is currently valuing tech companies. In 2026, the dominant question isn't "Are you growing?" but "Are you growing profitably?" Companies that can demonstrate expanding margins while riding the AI wave get rewarded. Companies that show revenue growth at the cost of margins get sold.

Cisco's networking segment illustrates this perfectly. Revenue jumped 21% year-over-year to $8.29 billion, comfortably beating the $7.9 billion estimate. That growth is directly tied to the AI infrastructure boom: hyperscalers and enterprise customers are building out networks at a pace not seen since the early cloud era. Cisco's switches, routers, and optical equipment are the plumbing that connects AI data centers, and demand is surging.

But the security segment told a different story. Revenue came in at $2.02 billion, missing the $2.11 billion estimate and declining 4% year-over-year. That's a segment where Cisco faces intense competition from pure-play cybersecurity firms like Palo Alto Networks and CrowdStrike, and the miss suggests that Cisco's diversification strategy isn't firing on all cylinders yet.

The full-year guidance miss is what really rattled investors. Cisco's outlook of $61.2 to $61.7 billion in revenue implies roughly 8.5% growth, which would be solid in any normal year. But Wall Street had been pricing in nearly $64 billion based on the assumption that AI-driven networking demand would accelerate through the back half of the fiscal year. A $2 billion gap between guidance and expectations signals either that Cisco is being conservative or that the company sees headwinds it isn't fully articulating yet.

The third-quarter guidance, which calls for revenue of $15.4 to $15.6 billion and earnings of $1.02 to $1.04 per share, was roughly in line with estimates. But "in line" isn't enough to repair confidence when the annual outlook disappoints. Markets want beats and raises, especially from companies positioned at the center of the AI infrastructure story.

AI's Hidden Supply Chain Tax

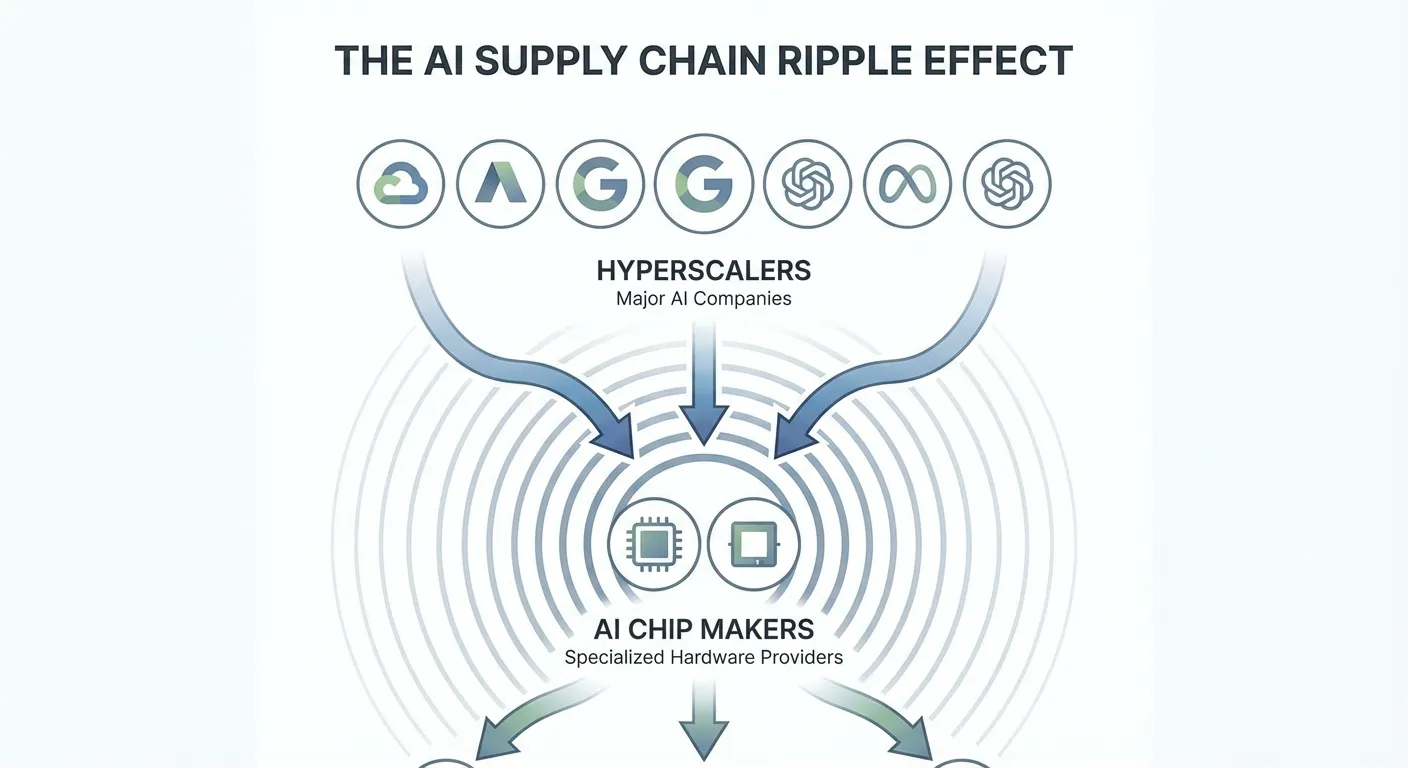

Cisco's situation is a window into a dynamic that's going to affect a lot more companies this earnings season. The AI spending boom is creating winners, but it's also creating hidden costs that ripple through supply chains in unexpected ways.

Consider the chain reaction. Hyperscalers order massive quantities of AI accelerators from Nvidia, AMD, and custom chip designers. Those accelerators require high-bandwidth memory from Samsung, SK Hynix, and Micron. The memory makers allocate production capacity toward their highest-margin customers, which are the AI chip makers. That allocation reduces supply for everyone else who needs memory chips: networking equipment makers, storage companies, automotive electronics manufacturers, consumer device producers.

The effect is a kind of inflationary tax on the broader tech ecosystem. Companies that are building AI infrastructure benefit from the boom directly. Companies that supply AI infrastructure, like Cisco, benefit from demand but pay more for inputs. And companies that have nothing to do with AI but compete for the same components, like AWS and others building custom silicon, face cost increases without the corresponding revenue boost.

Robbins framed Cisco's response as proactive. Raising prices and renegotiating contracts are standard tools for managing input cost inflation, but they carry risks: customers facing their own budget pressures may delay purchases or shift to competitors willing to absorb margins temporarily. In networking, where Cisco holds dominant market share but faces growing competition from Arista Networks and Juniper (now owned by Hewlett Packard Enterprise), pricing power isn't unlimited.

What Wall Street Missed and What It Got Right

The market's reaction to Cisco's earnings wasn't irrational, but it was arguably incomplete. The sell-off focused on the margin miss and the guidance gap while largely ignoring several genuinely positive signals.

Cisco's AI order pipeline exceeding $5 billion is significant. A year ago, Cisco was widely viewed as a legacy networking company that might get left behind by the AI wave. The Silicon One G300 chip launch and the company's growing role in AI data center connectivity suggest that narrative was premature. Cisco is becoming an AI infrastructure company whether Wall Street recognizes it or not.

The 21% networking revenue growth also deserves more credit than it received. That kind of acceleration in Cisco's largest segment indicates sustained enterprise demand that should provide a revenue floor even if margins remain pressured in the near term. Companies don't build out AI networks on a quarterly basis; these are multi-year infrastructure investments that create recurring revenue streams.

But Wall Street got one thing right: margin compression matters, especially when it's driven by structural supply chain dynamics rather than one-time factors. If memory chip prices remain elevated through 2026, and there's no reason to think they won't given the pace of AI infrastructure spending, Cisco's profitability challenge isn't going away next quarter. The company needs either to pass those costs through to customers faster or to shift its product mix toward higher-margin offerings that can absorb the input cost increases.

The Verdict

Cisco's quarter encapsulates the paradox of the current AI boom: the companies building the physical infrastructure that makes AI possible are seeing incredible demand, but the economics of that demand are more complicated than the headline revenue numbers suggest. Strong sales don't automatically translate to strong profits when the entire supply chain is being repriced around AI's voracious appetite for components.

For investors, the takeaway isn't that Cisco is in trouble. It's that the margin story matters more than the revenue story right now, and Cisco needs to demonstrate it can manage input costs without sacrificing the growth that makes it relevant in the AI era. The next quarter's margin number will be the one to watch.

For the broader tech sector, Cisco's earnings are a warning shot. If a company with Cisco's scale and market position is feeling the squeeze from memory chip inflation, smaller networking and infrastructure companies are feeling it worse. The AI boom's supply chain ripple effects are just beginning to show up in earnings reports, and Cisco won't be the last company to beat on revenue and disappoint on margins.

Sources

- Cisco's stock drops on mediocre forecast even as earnings and revenue top estimates - CNBC

- Cisco Stock Drops on Disappointing Revenue Outlook Despite Earnings Beat - Blockonomi

- Cisco revenue beats expectations, but margin outlook pressured by rising memory costs - Digitimes

- Cisco Systems Updates Q3 2026 Earnings Guidance - Daily Political