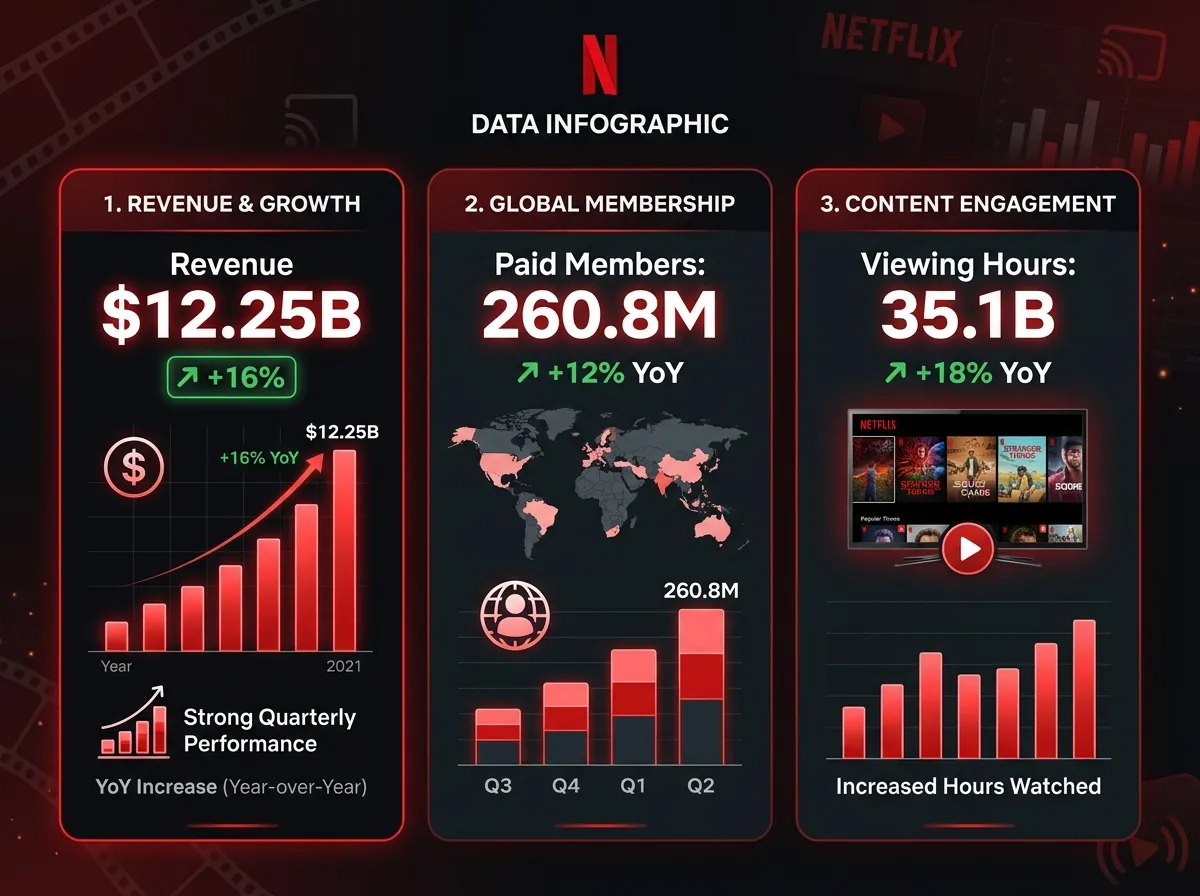

Netflix reported a near-clean quarter Thursday: $12.25 billion in revenue up 16%, earnings per share of $1.23 where analysts had penciled in 76 cents, net income of $5.28 billion, and free cash flow of $5.09 billion. Advertising revenue is still tracking toward a $3 billion annual run rate, double last year's number. By almost any normal reading, this should have been a bull's day.

The stock fell as much as 10% after the bell, opening Friday down 10.8% at $96.20. Two items explain the reaction, and neither is in the quarter that just closed. Netflix guided to a roughly 1.5 percentage point operating margin decline in Q2, and co-founder and chairman Reed Hastings said in the shareholder letter that he will leave the board in June, ending close to three decades of involvement with the company.

The combination, a soft near-term forecast and the departure of the person most associated with the company's identity, was enough to override everything else on the page.

What Actually Hit the Tape

The operating numbers were strong in every region. U.S. and Canada revenue grew 14% to $5.2 billion. Europe, the Middle East, and Africa grew 17% to $4 billion. Latin America grew 19% to $1.5 billion. Asia-Pacific grew 20%, led by Japan, where the World Baseball Classic drew 31.4 million Japanese viewers, becoming Netflix's most-watched title in that market and driving the single largest day of signups the service has ever had there.

The cash picture was even better than revenue suggested. Net income jumped 83% year over year. Free cash flow rose 91%. A meaningful piece of both, a pre-tax $2.8 billion, was the Paramount Skydance termination fee Netflix walked away with after its late-2025 bid for Warner Bros. Discovery fell apart and Paramount ultimately acquired the studio. The cash arrived in January, cleared the quarter, and will show up again only as a one-time item in year-over-year comparisons for the next three quarters.

The ad business, which Netflix co-CEO Greg Peters has spent three years building from nothing, now has more than 4,000 direct advertisers on the platform, up 70% from a year ago. Peters has told analysts for two years that the ad tier was approaching the scale where it can meaningfully move operating margins by late 2026. The Q1 numbers suggest he is on schedule. More than half of new signups in the first quarter chose the ad tier, continuing a trend that began in 2024, and the mix shift is a large part of why average revenue per member is flat even as the global subscriber base, which the company no longer breaks out quarterly, is still growing past the 325 million reported in January.

The Guidance That Spooked the Street

Then came the forecast. Netflix projected Q2 revenue growth of 13%, which is fine on its own, paired with an operating margin decline of about 1.5 percentage points relative to Q2 2025. Full-year 2026 guidance was reiterated, not raised, at $50.7 billion to $51.7 billion in revenue, with operating margins "around 32%." Wall Street had been pricing in a bump.

The price-hike math was the specific thing traders wanted addressed. Netflix pushed through tier increases across most markets in late March, too late to show up meaningfully in Q1 revenue. Analysts expected management to convert that pricing into a brighter full-year picture on Thursday. Peters instead said only that the company's typical pattern is for price-hike benefits to "layer in gradually." That is accurate historically, and also not the answer growth investors wanted in the hour.

Evercore ISI analyst Mark Mahaney, who maintained an Outperform rating with a $115 target, wrote that his long-term thesis on the stock is intact. "We don't view the Netflix long thesis as changed," Mahaney said in a Friday client note. "We continue to view Netflix as a high-quality asset." William Blair's Ralph Schackart was more pointed: "Netflix investors had a high bar, and the company did not meet it." Alicia Reese at Wedbush Securities, who raised her target to $118 going into the print and kept the Outperform rating, flagged a specific regional risk: "European resistance to price increases could be an overhang this year as Netflix works through legal challenges." Price cases in France and Germany are still being sorted out.

The bear note of the group came from Jeffrey Wlodarczak of Pivotal Research Group, who holds the stock at Hold with a $96 target. His framing was the one Netflix will hear more of. "Short-form entertainment is doing to streaming what streaming has done to traditional TV," he wrote. YouTube, TikTok, and Meta's Reels together now account for a larger share of U.S. screen time than any single subscription service, and the question of whether a 16% revenue grower on a mature base deserves a premium multiple is one the market is clearly less willing to answer yes to than it was a year ago.

Reed Hastings, Retiring From the Company Twice

The second news item was planted in the shareholder letter without fanfare. Reed Hastings, who co-founded Netflix in 1997, served as CEO until 2023, and has chaired the board since, will not stand for reelection at the June annual meeting. The disclosure is four sentences long. It closes an era that, depending on how you count, covers the DVD-to-streaming transition, the pivot to originals, the near-death cash crunch of 2011, the global expansion, the launch of the ad-supported tier, and the current post-peak-streaming consolidation that reshaped the rest of the industry.

Hastings has been public about his post-Netflix priorities since stepping down as co-CEO in 2023. He has accepted a board seat at Anthropic, the AI company, concentrated on philanthropy, and started a real estate project in ski country. His day-to-day fingerprints on Netflix have been faint since Ted Sarandos and Peters took over as co-CEOs.

None of which makes the exit immaterial. A founder leaving the board is the cleanest possible signal that the transition to the new regime is finished. Markets tend to read that as a loss of institutional memory at exactly the moment the company is making its most consequential bets in years, from live sports to the ad stack to the still-unsettled question of whether Netflix eventually buys or merges with a legacy studio after the Warner Bros. drama.

"It's a vote of confidence in the new leadership," Sarandos said on the call, which is the correct thing for a co-CEO to say. Investors sold anyway.

The Warner Bros. Shadow That Will Not Leave

The other thing hanging over the results is the collapsed Warner Bros. Discovery deal. Paramount Skydance's David Ellison outbid Netflix for Warner in a late-2025 process that saw Netflix lose, then benefit from, the $2.8 billion break fee. The legal and accounting structure was complicated. The strategic point is simpler. Netflix is the only company at its current scale without an owned legacy film and TV library to depreciate, merchandise, and repackage. It has built one internally, title by title, at enormous annual content cost. Paramount and Disney did not have to.

Sarandos has taken the position that this is a feature, not a bug, arguing publicly that Netflix wins or loses on what it makes now, not on what was made in 1952. The counterargument, which has become louder among analysts, is that streaming is increasingly a library-depth business in the second half of its life cycle. Thursday's reiterated guidance, rather than a raise, does not settle that debate. It leaves it live.

What the Ad Business Has to Deliver

Everything in the Netflix story now flows through the ad tier. Ad revenue is tracking toward $3 billion this year, still small compared to the roughly $51 billion top-line but the only growth line the company has that is not cost-capped by content spend or price-elasticity ceilings. If the ad business hits its trajectory, 2027 margins look very different than today's forecast. If it misses, the 32% full-year margin target starts to look like a ceiling rather than a floor.

Peters has built the ad platform largely in-house, with an assist from Microsoft's monetization stack. Netflix confirmed Thursday that its advertising DSP and measurement tools are now fully rolled out across all 12 ad markets, ending a buildout that started in late 2023. For a business that was zero in 2022, getting to $3 billion with 4,000 direct advertisers is a fast curve. The next doubling is going to require programmatic share and sports inventory, both of which Netflix is pursuing through partial rights deals rather than buying entire leagues.

The ad strategy is also the hedge against the bigger macro problem Wlodarczak named. If short-form video continues to take U.S. screen time, Netflix needs to extract more dollars per hour of watch time from the attention it still has. Advertising, not subscription, is the lever.

What This Quarter Actually Said

Strip the Hastings headline away and Thursday was a clean beat on top and bottom, a reiteration of the year, and a Q2 margin compression tied to content timing. Strip the Q2 guidance away and it is a beat on an already-high bar, with a founder transition that has been telegraphed for three years finally closing out.

What sits underneath the combined read is that the market is no longer paying the premium it once did for Netflix as the category killer. Price hikes are in. The ad business is on-plan but not ahead of plan. Hastings is out. The quarter was good. The next four will be judged on whether they are better, against a competitive set that now includes not just Disney, Paramount, and Amazon but short-form platforms the company cannot buy its way past.

Netflix reports Q2 in mid-July.

Sources

- Variety: Netflix Earnings Q1 2026 Revenue Up 16%, Beating Expectations

- CNBC: Netflix (NFLX) Q1 2026 earnings report

- Deadline: Netflix Q1 2026 Earnings: Revenue, Earnings Beat But Shares Still Plunge

- Hollywood Reporter: No Hike, No Hype: Netflix Stock Drops Absent 2026 Guidance Boost

- TipRanks: Wedbush Raises Netflix Stock Price Target Ahead of Q1 Earnings