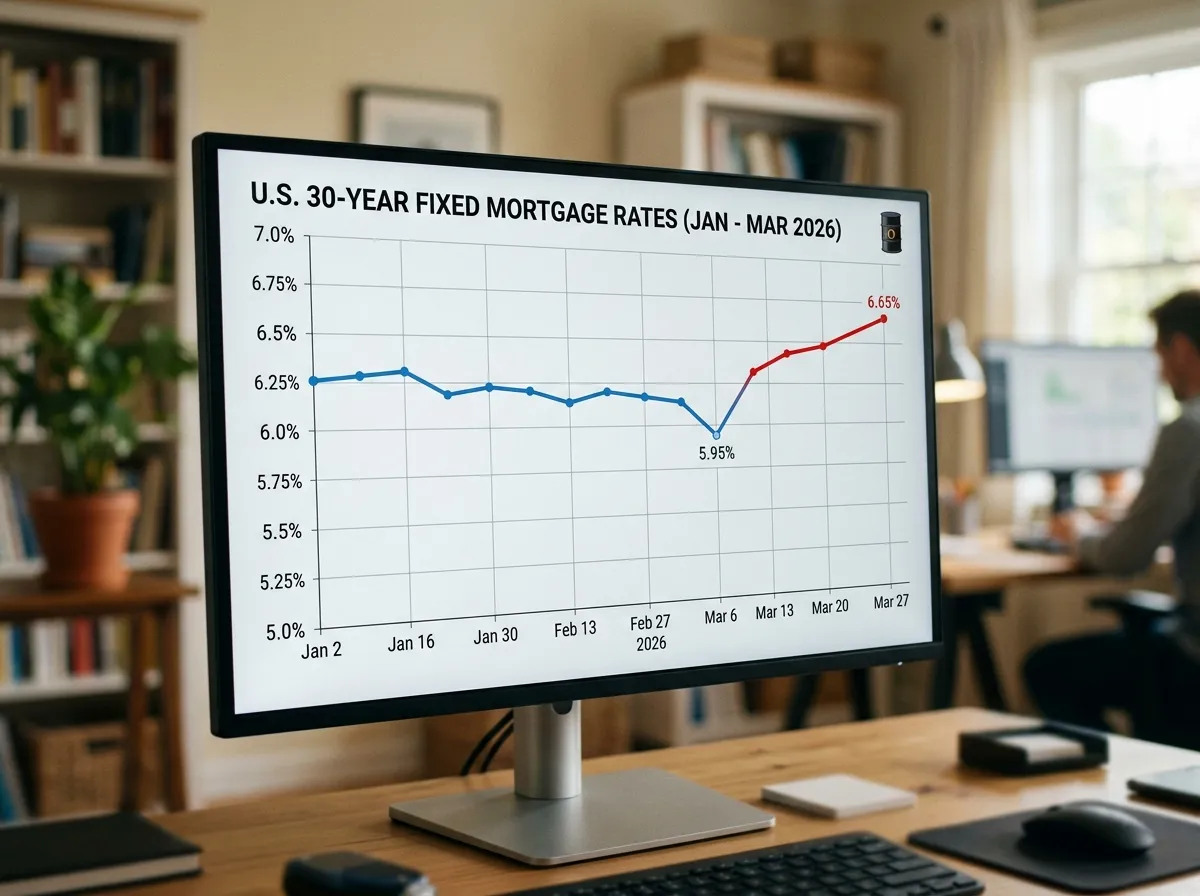

The first day of spring was supposed to mark the unofficial start of the 2026 housing recovery. Instead, it delivered a gut punch: the average 30-year fixed mortgage rate climbed to 6.53% on Friday, according to Mortgage News Daily, its highest level since late December. Just two weeks ago, rates had dipped below 6% for the first time since 2022, briefly giving buyers a glimpse of what an affordable spring season might look like. That window slammed shut, and the culprit isn't the Fed, the jobs market, or the usual suspects. It's oil.

The connection between crude prices and your monthly mortgage payment isn't obvious, but right now it's the single most important link in the housing market. Since the U.S.-Israeli strikes on Iran began February 28, Brent crude has surged from around $67 per barrel to above $103. That spike has reignited inflation fears, pushed Treasury yields higher, and dragged mortgage rates up by more than half a percentage point in under three weeks.

"The outlook for the spring homebuying season has become cloudier than it was even just a month ago," said Lisa Sturtevant, chief economist at BrightMLS.

How Oil Becomes Your Mortgage Problem

The chain from a blocked waterway in the Persian Gulf to the rate on your home loan runs through the bond market. When oil prices spike, investors expect higher inflation. Higher inflation expectations push up yields on the 10-year Treasury note, which is the benchmark for mortgage pricing. Lenders don't set rates based on the Federal Reserve's short-term rate alone: they price off Treasuries, and Treasuries right now are reacting to oil.

The Strait of Hormuz, through which roughly one-fifth of the world's crude oil flows, has been effectively closed to commercial traffic since early March. The disruption has erased years of progress toward energy price stability and sent shockwaves through global financial markets. The 10-year Treasury yield has climbed roughly 40 basis points since the conflict began, and mortgage rates have followed almost in lockstep.

The speed of the reversal has caught the housing industry off guard. In early March, when rates briefly dipped below 6%, mortgage applications surged and pending home sales rose 1.8%, according to data from the National Association of Realtors. The industry was gearing up for the strongest spring in years. Three weeks later, the math looks completely different.

The Math That's Keeping Buyers on the Sidelines

Half a percentage point might not sound like much. In dollar terms, it changes everything. On a $400,000 home with 20% down (a $320,000 loan), the difference between a 5.97% rate and a 6.53% rate adds about $120 per month to the payment, or roughly $43,200 over the life of a 30-year loan. For buyers already stretched by years of price appreciation and elevated rates, that margin is the difference between qualifying and walking away.

The numbers are showing up in real-time behavior. Mortgage applications fell 10% last week, according to the Mortgage Bankers Association, erasing gains from the brief sub-6% window. Refinance applications, which had surged when rates dropped, fell even harder. The National Association of Realtors' affordability index remains 35% below its pre-COVID level, and March's rate spike has only widened that gap.

Inventory, at least, is less of a problem than it used to be. Some 66 of the nation's 200 largest housing markets now have active listings above pre-pandemic 2019 levels, according to ResiClub Analytics, with Sun Belt markets like Austin, Phoenix, and Tampa leading the way. But more homes on the market don't help buyers who can't afford the monthly payments. The supply side was finally cooperating just as the demand side got crushed.

What the Fed Can and Can't Do

Wednesday's Federal Reserve meeting offered no relief. Chair Jerome Powell held rates steady, noting the "uncertain" impact of the conflict on the economy. The Fed is stuck in a familiar bind: cutting rates could fuel inflation at a moment when energy prices are already pushing costs higher, while holding rates steady does nothing to help a housing market that was just beginning to thaw.

The central bank's language was carefully hedged, acknowledging both the risk of an oil-driven inflation resurgence and the possibility that the conflict's economic drag could ultimately warrant easing. Markets are currently pricing in one rate cut by July, but that expectation shifts daily based on headlines from the Middle East.

Powell's options are limited in a way they haven't been since the post-pandemic inflation surge. The housing market's recovery was built on the assumption that rates would gradually decline throughout 2026, and that assumption depended on inflation continuing to cool. Oil prices have introduced a variable the Fed can't control, and every week the Strait of Hormuz stays closed makes the mortgage picture worse.

Two Scenarios for the Spring Season

The housing market's trajectory from here depends almost entirely on how long the Iran conflict lasts and whether oil prices stay above $100. Economists are broadly sketching two paths.

If the conflict winds down by mid-April: Oil prices retreat toward $80-85 per barrel, Treasury yields ease, and mortgage rates drift back toward 6% by May. The spring buying season gets a late start but still records modest gains in sales volume. This is the scenario most Wall Street forecasters publicly hope for, even if few are confident enough to bet on it.

If the conflict persists into summer: Oil stays above $100, inflation expectations become entrenched, and the Fed delays any rate cuts until September or later. Mortgage rates could test 6.75% or higher, effectively killing the 2026 housing recovery before it starts. Construction starts, already sluggish, would slow further as builders lose confidence in buyer demand.

"If you're a buyer who's been waiting for the right moment, this isn't it, but it might not get better before it gets worse," Sturtevant told reporters. "The window that opened briefly in early March was real, and it closed faster than anyone expected."

The Verdict

The cruelest irony of the 2026 spring housing market is its timing. After four years of elevated rates, limited inventory, and declining affordability, the pieces were finally falling into place. Rates were dropping. Inventory was rising. Builders were building. Then a geopolitical crisis 7,000 miles away rewrote the math in three weeks.

For prospective buyers, the practical calculus hasn't changed: if you find a home you can afford at today's rates, the purchase still makes sense long-term. What has changed is the ceiling of uncertainty. The spring market isn't dead, but its recovery depends entirely on events no economist, policymaker, or buyer can control. The oil market, not the housing market, is setting mortgage rates right now, and that's unlikely to change until the Strait of Hormuz reopens.