Three weeks ago, the Federal Reserve's path looked clear. Inflation was cooling. The job market was stable. Two or three rate cuts in 2026 seemed like a safe bet, and markets had priced them in with near certainty. Then the United States and Israel launched strikes on Iran on February 28, and the math changed overnight.

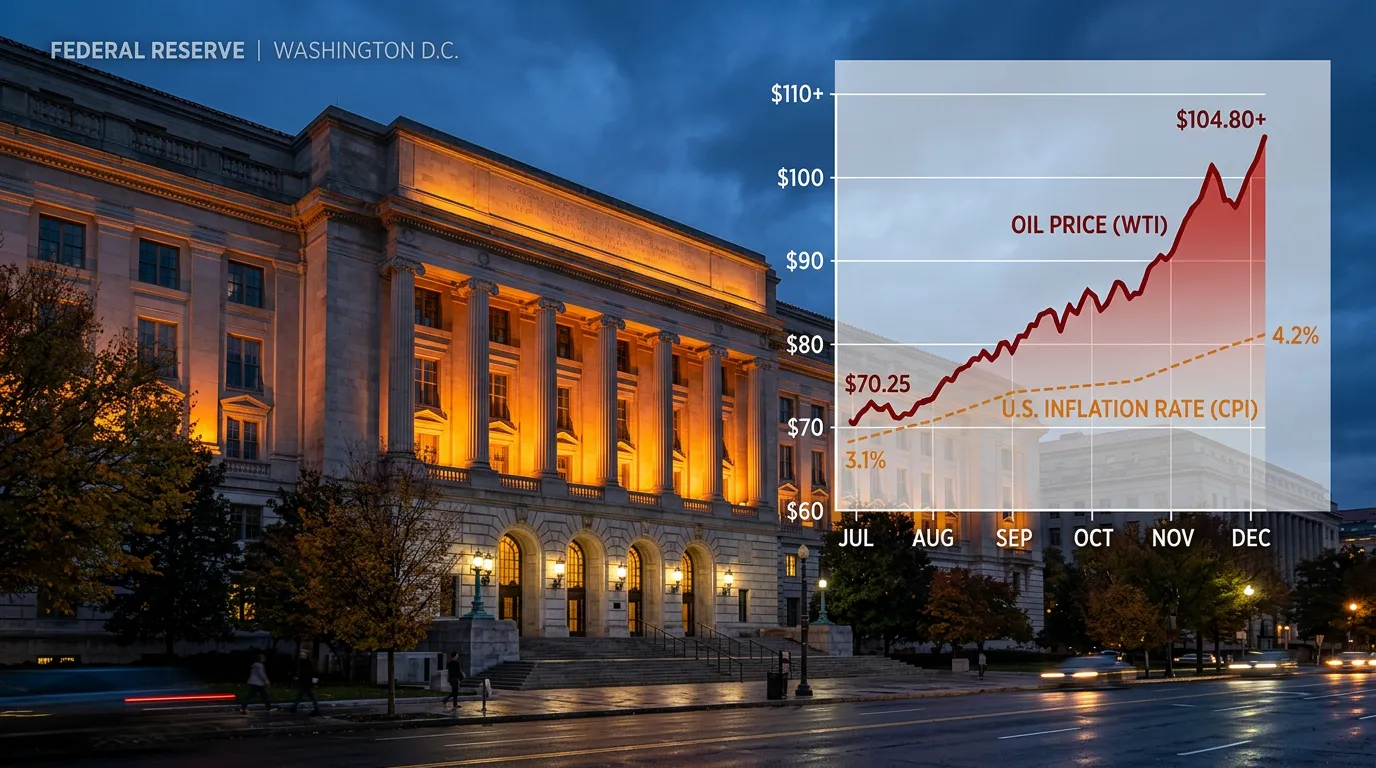

As the Fed begins its two-day policy meeting on Tuesday, Brent crude sits above $106 per barrel, West Texas Intermediate hovers near $102, and the national average gas price has surged to $3.72 a gallon, up nearly 80 cents in less than a month. The Strait of Hormuz, responsible for roughly 20% of global seaborne oil, is operating at less than 10% of its pre-conflict capacity. And the International Energy Agency has already pulled the trigger on the largest emergency oil reserve release in history, 400 million barrels, without managing to push prices back below triple digits.

The Fed's decision on Wednesday afternoon is almost certain to be a hold at 3.50% to 3.75%. Traders on the CME FedWatch tool are pricing in a 98.9% probability of no change. But the real story isn't what happens this week. It's what Chair Jerome Powell says about what comes next, and whether the central bank can thread a needle that keeps getting smaller.

A Supply Shock the Fed Can't Fix

The core problem for the Federal Reserve is one of taxonomy. Not all inflation is the same, and monetary policy tools are designed for one kind but largely helpless against another. When consumers spend too much and prices rise because demand outstrips supply, higher interest rates cool the economy by making borrowing more expensive. That's demand-pull inflation, and the Fed has the playbook for it.

What's happening now is different. The Iran war has physically removed oil supply from the global market. Tanker traffic through the Strait of Hormuz has collapsed. That's a supply shock, and raising interest rates doesn't produce more oil, reopen shipping lanes, or resolve a military conflict. If anything, tightening monetary policy during a supply shock risks compounding the damage by slowing an economy that's already absorbing higher energy costs.

"The Fed is in a classic bind," said Mark Zandi, chief economist at Moody's Analytics, in a CNBC interview on March 12. "They can't cut rates because inflation expectations are moving higher. They can't raise rates because the economy is already slowing under the weight of $100 oil. So they sit, and they hope it resolves before they're forced to choose."

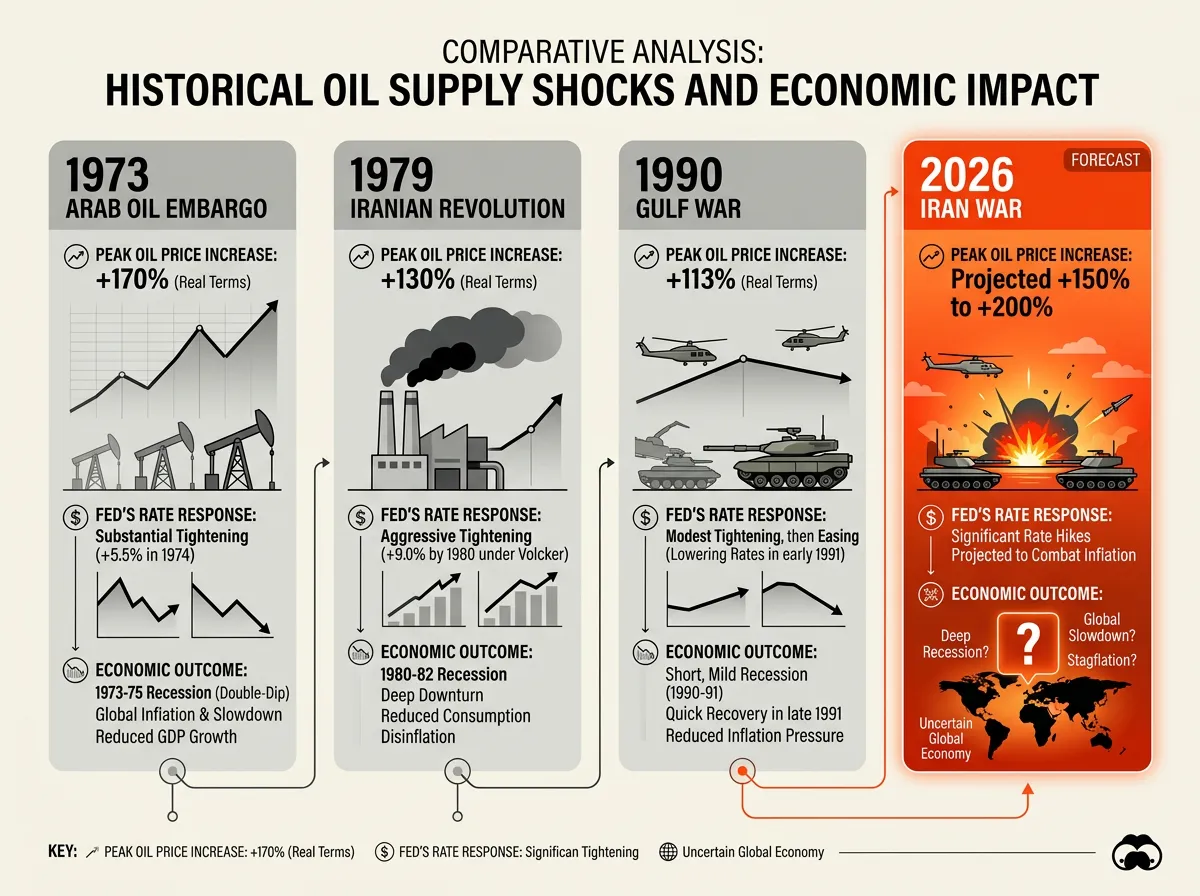

The historical precedents aren't comforting. The 1973 Arab oil embargo led to stagflation that lasted nearly a decade. The 1979 Iranian Revolution triggered a second oil shock that pushed inflation above 14% and required Paul Volcker's punishing rate hikes to break. Even the milder 1990 Gulf War oil spike contributed to a recession. In each case, the Fed had to decide whether fighting inflation or supporting growth mattered more, and in each case, the choice came with significant economic pain.

The Inflation Numbers That Keep Powell Up at Night

February's Consumer Price Index, released on March 11, showed headline inflation at 2.4% year-over-year, essentially unchanged from January. On the surface, that looks manageable. But the February data captures only the first few days of the oil shock, since prices didn't start spiking until the strikes began on February 28.

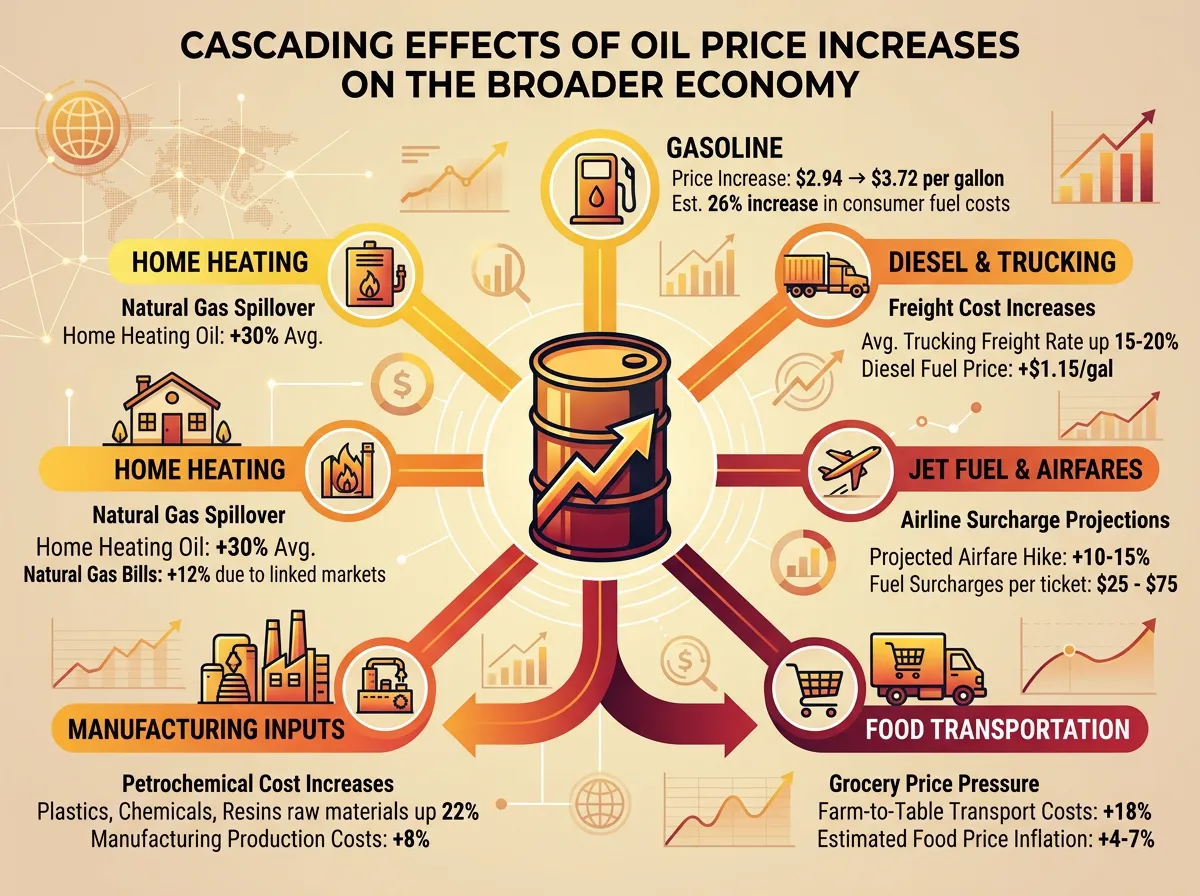

The March CPI report, due in mid-April, will tell a far more alarming story. Gasoline prices have surged 26.9% over the past month, the largest monthly increase since Hurricane Katrina, according to NPR's reporting on March 16. Diesel is approaching $5 a gallon, up $1.34 from a month ago. Those fuel costs ripple through everything: trucking, shipping, manufacturing, food production.

RBC Economics published an analysis warning that if oil stays above $100 per barrel through Q2, headline CPI could climb to 3.5% by summer. That would represent a meaningful reversal from the disinflationary trend the Fed has spent two years cultivating. More critically, it could unanchor inflation expectations, the psychological threshold where businesses and consumers start pricing in higher future inflation, making it self-fulfilling.

The University of Michigan's consumer sentiment survey, released March 14, showed one-year inflation expectations jumping to 4.1%, up from 3.1% in February. That's the kind of move that gets the Fed's attention fast. Once expectations become unmoored, bringing them back requires aggressive rate action that almost always triggers a recession.

"The Fed's nightmare scenario isn't $100 oil," said Julia Coronado, founder of MacroPolicy Perspectives and a former Fed economist. "It's $100 oil combined with 4%+ inflation expectations. That's when you lose the luxury of patience."

Why Rate Cut Hopes Are Evaporating

Before the Iran war, financial markets were pricing in two to three quarter-point rate cuts in 2026, with the first expected as early as June. That consensus has disintegrated in under three weeks.

Goldman Sachs pushed its forecast back on March 10, now expecting quarter-point cuts only in September and December, citing elevated inflation risks tied to the oil shock. But even that revised outlook may be optimistic. As of Monday, futures markets have taken a September cut entirely off the table. Traders now see just one cut, likely in December, with no additional reductions priced in until well into 2027 or possibly early 2028.

The shift has real consequences for anyone with a mortgage, car loan, or credit card balance. The federal funds rate at 3.50% to 3.75% translates into mortgage rates that have climbed back above 7% after briefly dipping below 6.5% in January. Auto loan rates are averaging 7.8% for a 60-month new car loan, according to Bankrate data. Credit card APRs remain at all-time highs near 21%.

For the housing market, the timing is particularly painful. The spring buying season typically picks up in March and April, but 7%+ mortgage rates have frozen many potential buyers and sellers in place. The National Association of Realtors reported that existing home sales in February fell 4.2% month-over-month, and the oil-driven rate recalculation threatens to extend the housing market's two-year slump.

Powell's Tightrope: What to Listen for Wednesday

The rate decision itself will be uneventful. The real information will come from two sources: the updated Summary of Economic Projections (the "dot plot") and Powell's press conference at 2:30 PM ET on Wednesday.

The dot plot will show where each of the 19 Fed officials expects rates to be at the end of 2026 and 2027. In December, the median projection called for two quarter-point cuts this year, bringing rates to 3.00% to 3.25%. If that median shifts to one cut or zero, markets will take it as confirmation that the Fed's easing cycle is effectively on pause.

Powell's language will matter even more than the dots. Market participants will be parsing every word for signals on three questions. First, does the Fed view the oil shock as transitory (a word Powell has learned to use carefully) or persistent? If Powell frames it as a temporary supply disruption likely to resolve when the conflict ends, that signals the Fed is willing to look through higher energy prices and resume cutting later this year. If he describes it as a risk to the inflation outlook that requires monitoring, that's Fed-speak for "cuts are off the table until we see where this goes."

Second, how does the Fed assess the risk to economic growth? Consumer spending has held up so far, but the full impact of higher gas and energy costs hasn't filtered through yet. If Powell mentions downside risks to growth or the possibility of a slowdown, markets may interpret that as the Fed being open to preventive cuts even with elevated inflation, a scenario that would be bullish for stocks and bonds.

Third, what's the Fed's view on the IEA's 400-million-barrel reserve release? The unprecedented coordinated release was designed to stabilize prices, but crude has stayed stubbornly above $100 despite the announcement. If Powell acknowledges that supply-side interventions haven't been sufficient, it raises the stakes for what the Fed might eventually need to do on its own.

The Stagflation Question Nobody Wants to Ask

The word that keeps surfacing in analyst notes and economic commentary is one that hasn't been relevant for four decades: stagflation. It describes an economy experiencing stagnant growth and rising inflation simultaneously, a combination that makes conventional policy responses counterproductive. Raise rates to fight inflation, and you deepen the slowdown. Cut rates to support growth, and you risk letting inflation spiral.

The U.S. isn't there yet. GDP growth in Q4 2025 came in at an annualized 2.3%, and the labor market added 187,000 jobs in February. Those aren't recession numbers. But the Atlanta Fed's GDPNow model, which tracks real-time economic data to estimate current-quarter growth, has been declining steadily since the conflict began. As of March 14, the model projects Q1 2026 GDP growth at 1.1%, down from 2.0% at the start of the month.

The bottom 60% of income earners devote close to 4% of their take-home pay to gasoline, according to the Bureau of Labor Statistics, roughly double the share for the top 10%. Every 50-cent increase at the pump acts as a regressive tax, pulling money away from discretionary spending and into fuel tanks. If consumers start cutting back on restaurants, retail, and travel in response, the growth side of the ledger deteriorates further.

Mohamed El-Erian, chief economic adviser at Allianz, wrote in a Financial Times column on March 14 that the Fed faces "the most complex policy environment since the 1970s." He argued that the central bank should prioritize inflation credibility even at the cost of near-term growth, because losing control of inflation expectations would ultimately be more damaging than a mild recession.

Not everyone agrees. Former Treasury Secretary Lawrence Summers argued on Bloomberg Television that the Fed should signal willingness to cut rates if growth deteriorates sharply, warning that the global economy is more fragile than headline numbers suggest and that "the risk of policy error on the too-tight side is at least as large as on the too-loose side."

What This Means for Your Money

If you're waiting for interest rates to come down before making a financial move, you may be waiting longer than you planned. Here's what the Fed's paralysis means in practical terms.

Mortgages are unlikely to drop meaningfully until late 2026 at the earliest. If you're shopping for a home, the 6% mortgage rate environment that seemed plausible in January is probably not coming back this year. Plan for 7% and hope to be pleasantly surprised.

Savings rates are the silver lining. High-yield savings accounts and CDs are still offering 4.5% to 5.0% APY. With the Fed holding steady, those rates should persist for months.

Gas prices are the most immediate hit to household budgets. The national average is $3.72 and trending higher. Analysts at GasBuddy project a peak somewhere between $4.00 and $4.50 if the Strait of Hormuz remains disrupted, with California potentially seeing $6+ at the pump. Adjusting driving habits, consolidating errands, and evaluating commute alternatives can provide real savings at these levels.

The stock market has been surprisingly resilient, with the S&P 500 closing at 6,716 on Tuesday, up 0.25%. But energy-sensitive sectors like airlines, trucking, and consumer discretionary remain under pressure. Investors with diversified portfolios that include energy exposure have been partially hedged against the oil spike, since energy stocks have rallied 18% since the conflict began.

The Waiting Game That Could Last All Year

The uncomfortable reality is that the Fed's decision on Wednesday isn't really a decision at all. It's an acknowledgment that the central bank is stuck, unable to ease policy because inflation is rising and unwilling to tighten because growth is slowing. The geopolitical pressures reshaping Cuba's economy this week offer a glimpse of what happens when energy crises go unresolved for too long. The institution that markets look to for direction is essentially saying: we don't know yet, and we need more time.

That's not a comfortable message for anyone managing a household budget, a business, or a portfolio. But it may be the most honest one. The NVIDIA GTC conference this week reminded markets that the AI-driven investment boom continues to provide one engine of economic growth. And the IEA's reserve release, while insufficient so far, is a coordinated global response that didn't exist in previous oil crises.

What happens next depends almost entirely on the Strait of Hormuz. If the military situation de-escalates and shipping resumes, oil drops back toward $70 to $80, the Fed resumes cutting by summer, and this episode becomes a footnote. If the blockade persists or the conflict widens, the Fed faces the kind of impossible choice it hasn't confronted since Volcker raised rates to 20% in 1981.

Powell will likely try to keep both options open on Wednesday. His challenge is convincing markets that patience is a strategy, not a stall. For the 158 million Americans filling up their gas tanks this month, patience isn't a luxury. It's a cost, and it's climbing by the day.

Sources

- NPR: Gasoline Prices Are Still Rising as the Iran War Stretches Into Its Third Week

- CNBC: Markets' Hopes for Fed Interest Rate Cuts Are Rapidly Fading Away

- CNBC: The Biggest Release of Emergency Oil Stockpiles in History Was Announced. Why Crude May Keep Rising

- CBS News: Iran War Is Making It Harder for the Federal Reserve to Cut Interest Rates

- NBC News: U.S. Oil Soars Past $100 a Barrel, as Iran War Shows No Signs of Ending Soon