Netflix just lost a bidding war it was supposed to win, and the entertainment industry will never look the same.

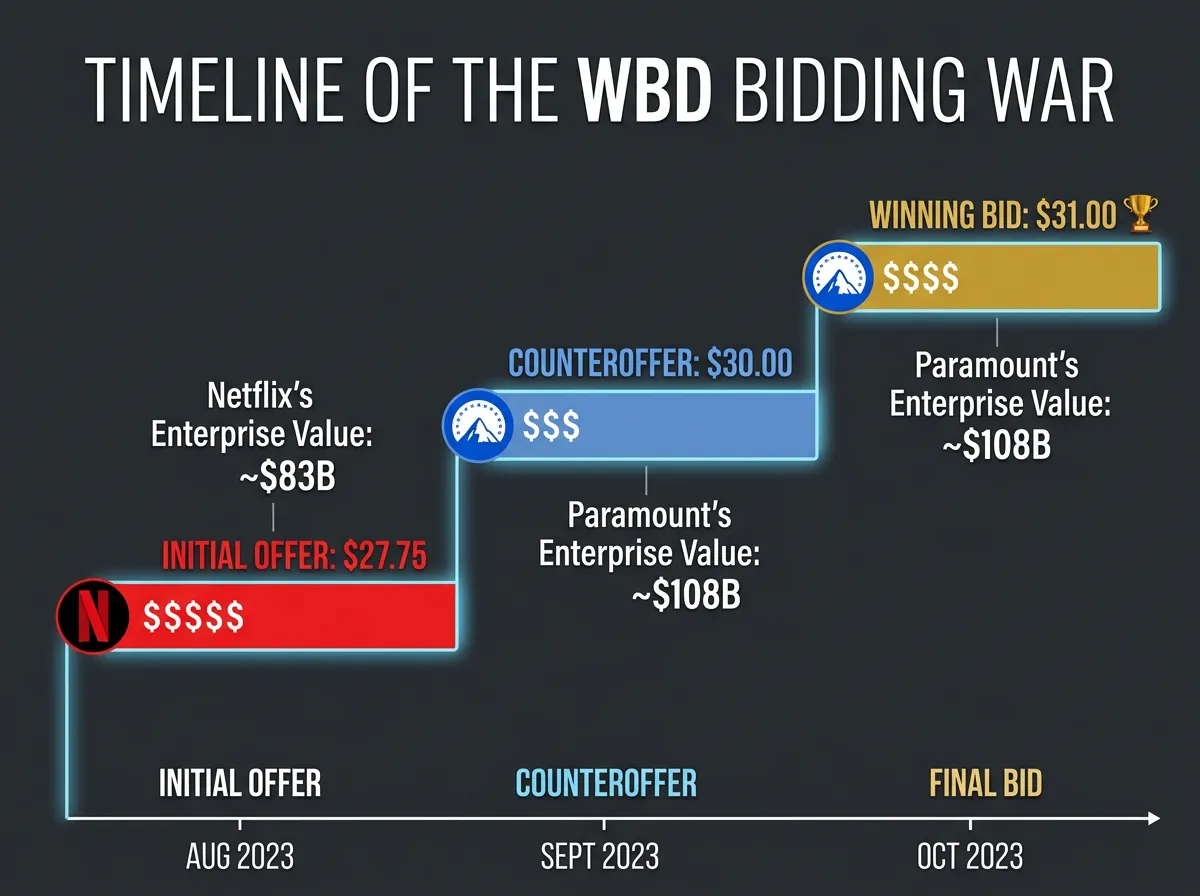

On Wednesday evening, Warner Bros. Discovery's board declared Paramount Skydance's revised offer of $31 per share "superior" to the existing Netflix deal, triggering a four-day matching period that Netflix promptly declined to use. CEO Ted Sarandos confirmed Thursday that Netflix would not increase its bid, stating that "at the price required to match Paramount Skydance's latest offer, the deal is no longer financially attractive." With that single sentence, the largest entertainment merger in history moved from contested to all-but-certain. Paramount Skydance will acquire the entirety of Warner Bros. Discovery for approximately $111 billion, creating a media conglomerate that controls CBS, CNN, HBO, Paramount Plus, Discovery Channel, Nickelodeon, Comedy Central, TBS, TNT, HGTV, and two of Hollywood's most storied film studios.

David Ellison, the 42-year-old CEO of Paramount Skydance and son of Oracle co-founder Larry Ellison, is about to become the most powerful person in entertainment. The question now is whether that power will survive Washington's antitrust regulators.

How a $27.75 Offer Became a $111 Billion Takeover

The path to this moment has been one of the most complicated corporate dramas in recent Hollywood history, a saga that involved hostile bids, political lobbying, and a chess match between two of the world's richest companies.

It started in late 2025, when Netflix struck a deal to acquire Warner Bros. Discovery's studios, streaming service, and intellectual property for $27.75 per share. The deal made strategic sense for Netflix: it would bring HBO's prestige content library, Warner Bros.' film slate, and the Discovery Channel's unscripted programming under the Netflix umbrella. For WBD's shareholders, who had watched the stock crater since the ill-fated Discovery-WarnerMedia merger in 2022, the offer was a lifeline.

Then Paramount Skydance showed up uninvited. In December 2025, just weeks after Ellison's company completed its own contentious merger with Paramount Global, it launched a hostile bid for WBD at $30 per share. The move stunned the industry. Paramount had barely finished integrating Skydance's operations, and here was Ellison reaching for the other major legacy media company still standing.

Over the following months, the two sides escalated. Netflix's initial agreement included exclusivity protections, but Paramount's persistent bidding forced WBD's board to engage. When Paramount raised its offer to $31 per share on February 25, the math shifted. WBD's board had a fiduciary obligation to pursue the higher offer, and they did.

What $111 Billion Actually Buys

The combined Paramount-WBD entity would control an extraordinary concentration of entertainment assets. On the film side alone, the company would own both Paramount Pictures and Warner Bros. Pictures, two studios that between them produced The Godfather, Top Gun: Maverick, Barbie, Harry Potter, and Mission: Impossible. The combined film library is arguably the deepest in Hollywood.

On the television and streaming front, the company would operate Paramount Plus, HBO and its Max streaming platform, Discovery Plus, and the linear networks CBS, CNN, TNT, TBS, Comedy Central, Nickelodeon, HGTV, and the Discovery Channel family of networks. In practical terms, this means a single company would control CBS evening news, CNN's cable coverage, HBO's prestige drama, Nickelodeon's children's programming, Discovery's reality slate, and Paramount's film pipeline.

The financial architecture of the deal is equally significant. Paramount's amended offer carries an enterprise value of approximately $108 billion and is "fully financed," according to regulatory filings. Larry Ellison and RedBird Capital Partners have committed $43.6 billion in equity, while Bank of America, Citigroup, and Apollo are providing $54 billion in debt commitments. Paramount will also assume WBD's existing $33 billion in debt. The total financial obligation is staggering by any measure.

Paramount has also agreed to pay the $2.8 billion termination fee that WBD owes Netflix for breaking their original deal, plus a $7 billion regulatory breakup fee if antitrust authorities block the merger. That $7 billion figure is unusually large, signaling both Paramount's confidence in regulatory approval and its willingness to absorb enormous risk.

Why Netflix Walked Away

Netflix's decision to step back is the most revealing part of this story. The company that spent the last decade disrupting traditional media decided that owning traditional media wasn't worth the price.

Sarandos' explanation was deliberately understated. Netflix looked at the $31 per share threshold, ran the numbers on what it would cost to absorb WBD's debt, restructure its operations, and integrate its workforce, and concluded the deal no longer met its financial standards. For a company that built its empire on original content and algorithmic recommendation rather than legacy libraries and cable network bundles, paying a premium for CNN, HGTV, and a collection of aging linear TV properties may have looked more like a burden than a bargain.

There's also a strategic dimension that Sarandos didn't say publicly but that analysts have noted. Netflix's original play was never about owning WBD as a whole. It wanted HBO's content library and Warner Bros.' film studio, the premium assets that would strengthen its streaming platform. The linear television networks, the news division, and the unscripted cable channels were overhead that Netflix would have needed to manage, spin off, or wind down. At $27.75 per share, the premium assets justified the overhead. At $31, they didn't.

The Ellison Factor: Tech Money Reshaping Hollywood

David Ellison's ascent to entertainment kingmaker has been rapid and unconventional. A year ago, he was the founder of Skydance Media, a production company known for co-financing Top Gun: Maverick and Mission: Impossible sequels. His company was respected but relatively small by studio standards. Then came the Paramount merger in August 2025, a deal that itself was contentious, involving lawsuits from shareholders and a controversial $16 million settlement with the Trump administration over editing at CBS's 60 Minutes.

Now Ellison is attempting to build what would functionally be the largest entertainment company on earth, backed by his father's fortune. Larry Ellison, whose net worth exceeds $200 billion through his Oracle holdings, has made an "irrevocable personal guarantee" of $40.4 billion toward the WBD acquisition, according to Variety. This isn't a leveraged buyout by a private equity firm looking to strip assets and flip properties. This is a tech billionaire's son using his family's generational wealth to rebuild Hollywood's corporate structure from the ground up.

The political dimension complicates the picture. NPR reported that both Ellisons maintain warm ties to Trump administration officials, and Ellison has argued that regulatory approval would be smoother under the current administration. Meanwhile, Netflix's Sarandos reportedly met with White House officials on Thursday to advocate for his company's position. When the approval process for an entertainment merger involves competing lobbying efforts in Washington, it says something about how thoroughly politics and media have become intertwined.

The Regulatory Gauntlet Ahead

The merger's HSR (Hart-Scott-Rodino) waiting period expired on February 19, meaning federal antitrust regulators have had their initial look at the deal. But California Attorney General Rob Bonta issued a pointed statement calling the merger "not a done deal" and warning that it faces significant antitrust scrutiny.

The concerns are obvious. A single company controlling CBS, CNN, HBO, Nickelodeon, Paramount Plus, and multiple cable networks would hold enormous leverage over distributors, advertisers, and competitors. The combined entity's market share in filmed entertainment, when calculated alongside its streaming footprint, would exceed any single company in Hollywood history.

European regulators will also need to approve the deal, adding another layer of scrutiny. The EU has historically been more aggressive than the US on media concentration, and a combined Paramount-WBD would have a significant presence in European markets through distribution deals and local content production.

That $7 billion regulatory breakup fee isn't just insurance. It's an acknowledgment that the antitrust fight could be real and prolonged. If regulators demand significant divestitures, stripping off CNN or spinning out cable networks, the economics of the deal change substantially. Ellison is betting that the current political environment favors large mergers, but regulatory environments shift, and this deal will take months to close.

The Bigger Story

This merger, if completed, would mark the definitive end of the streaming wars as we've known them. For the past decade, the entertainment industry's central narrative has been fragmentation: every major media company launching its own streaming service, competing for subscribers, and bleeding cash to build content libraries. Disney Plus, Paramount Plus, HBO Max, Peacock, Discovery Plus, Apple TV Plus, and Netflix all chased the same subscribers with the same strategy. The result was a content glut, subscriber fatigue, and billions in losses for nearly everyone except Netflix.

What's happening now is the opposite: consolidation. Paramount already absorbed Skydance. Now it's absorbing Warner Bros. Discovery. Disney has been exploring its own strategic options. The next era of entertainment won't be defined by how many streaming services exist. It will be defined by how few.

For consumers, the implications are mixed. A larger combined library could mean better value on a single subscription, fewer overlapping services, and less confusion about where to find specific content. It could also mean higher prices, reduced competition, and fewer creative risks from studios that no longer need to differentiate themselves from rivals. When two studios become one, the market for scripts, talent deals, and independent production narrows.

For the industry's workforce, the calculus is grimmer. Entertainment mergers historically produce significant layoffs as redundant departments are consolidated. Warner Bros. Discovery already cut thousands of jobs after its 2022 merger. A second consolidation would likely trigger another round, particularly in corporate, marketing, and distribution roles that exist in duplicate across both companies.

The biggest question may be the simplest one: can David Ellison actually run all of this? Producing Top Gun: Maverick and managing CBS, CNN, HBO, Nickelodeon, two film studios, multiple streaming platforms, and a $33 billion debt load are different challenges by several orders of magnitude. Hollywood has a long history of ambitious consolidators who built empires that collapsed under their own weight. Ellison has tech money, political connections, and a family fortune backing him. Whether he has the operational judgment to make this work is the $111 billion question that won't be answered for years.

Sources

- Netflix ditches deal for Warner Bros. Discovery after Paramount's offer is deemed superior - CNBC

- In reversal, Warner Bros. jilts Netflix for Paramount - NPR

- Paramount Skydance Clinches Warner Bros. Discovery in $111 Billion Mega-Merger - FinancialContent

- Larry Ellison Has Made 'Irrevocable Personal Guarantee' of $40.4 Billion Toward WBD Bid - Variety

- Paramount Comments on WBD Board's Determination of Superior Proposal - PR Newswire