Americans have placed more than half a trillion dollars in sports bets since 2018. Now the bill is coming due, and it's showing up on their credit reports. A new study from the Federal Reserve Bank of New York found that legalized sports betting is driving a measurable rise in credit delinquencies across the country, with the sharpest damage concentrated among people under 40. The findings arrive just as March Madness wraps up a record-setting season: Americans were projected to wager $3.3 billion on this year's tournament alone, a 50% jump over three years.

The research, published in March on the NY Fed's Liberty Street Economics blog, analyzed transaction-level consumer spending data alongside a nationally representative sample of Equifax credit records. The conclusion is blunt. In states where sports betting is legal, credit delinquency rates, meaning payments more than 90 days overdue, rose by about 0.3 percentage points across the overall population. That might sound modest. It is not. Among the roughly 3% of the population who actually started betting after their state legalized it, delinquencies spiked by more than 10%.

For younger bettors, the picture is even worse.

The Numbers Behind the Damage

The NY Fed study, authored by former research analyst Jacob Goss and research economist Daniel Mangrum, paints a detailed portrait of how quickly legal betting reshapes spending habits and financial health.

Here's what the data shows:

- Betting spending more than doubled. Average quarterly deposits went from under $500 in December 2019 to over $1,000 by June 2021. By 2025, quarterly deposits had climbed to roughly $1,250.

- Credit card delinquencies among bettors under 40 surged 26%. Across all ages, the delinquency increase was 10%, but younger adults bore a disproportionate share.

- Credit card delinquency rose by 1.02 percentage points for those under 40. Auto loan delinquency jumped 0.55 percentage points for the same age group.

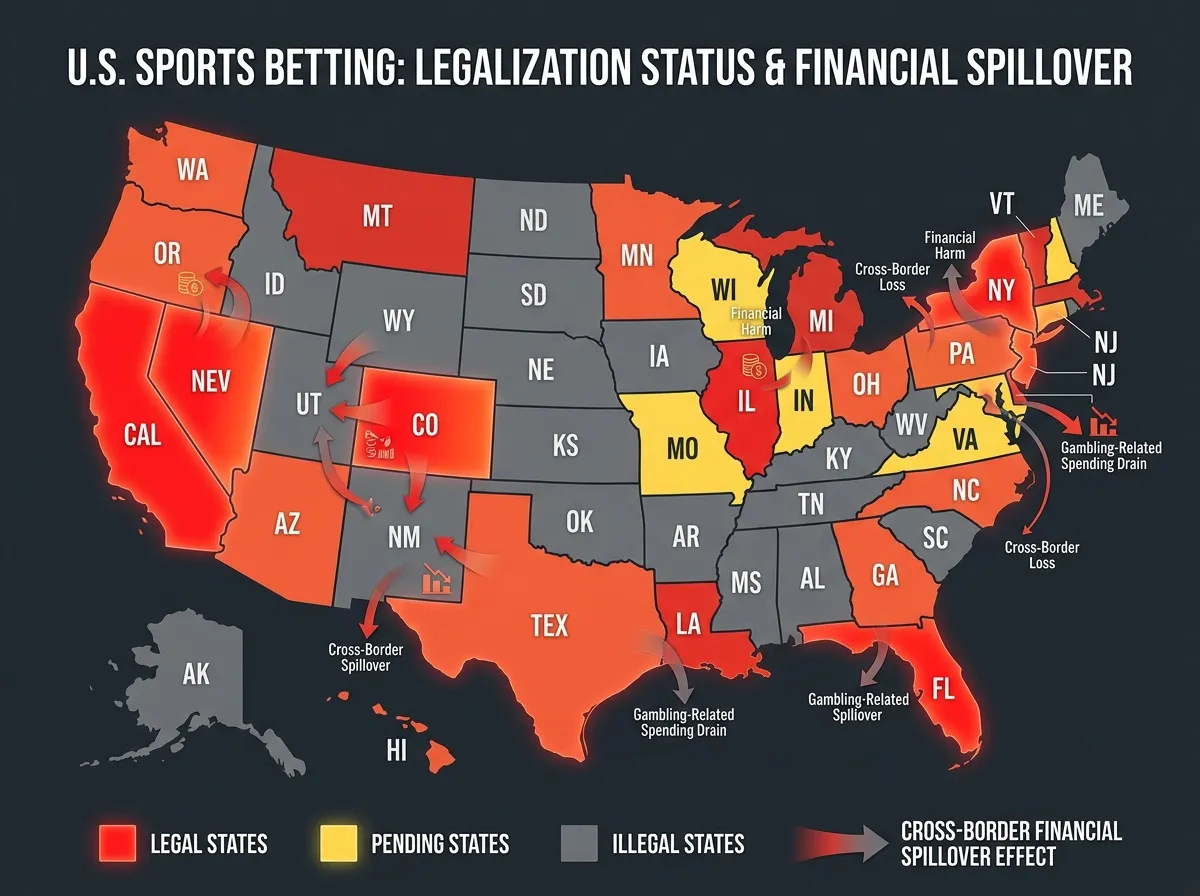

- The damage crosses state lines. Counties within 15 miles of a legal-betting state saw delinquency rise by about 0.2 percentage points, roughly 15% of the direct effect seen in legal states.

The spending growth has plateaued per bettor since 2022, but the total keeps climbing because more people keep signing up. Nearly 50% of men ages 18 to 49 now have an online sportsbook account. Commercial gaming revenue hit $78.7 billion in 2025, a 9.2% increase over the prior year.

Who's Getting Hurt the Most

The NY Fed findings line up with a broader body of research pointing at the same vulnerable population: younger adults, especially men. A 2024 National Bureau of Economic Research paper found that household bets increased by $1,100 annually in states with legal online sports betting, paired with a 14% decrease in net investments. People aren't just losing money on bets. They're pulling funds out of savings and investment accounts to keep gambling.

And the industry knows exactly where its profits come from. One gambling company's disclosures revealed that 70% of its profits came from less than 1% of its users. That's not a customer base. That's a dependency model.

Christopher Welsh, an addiction psychiatrist at the University of Maryland, told NPR the nature of the problem has shifted dramatically. "It's not like the other forms of gambling," Welsh said. "We're still getting calls about casino gambling, but it's almost all online sports betting now."

Welsh described a pattern that families often don't see coming. "We're getting more calls from even parents of college kids," he said. "They have no idea anything is going on, and then they're getting a call from a bookie." The debts compound quickly because bettors chase losses with borrowed money. "With gambling, it's almost always people are resorting to getting money from other sources to do it," Welsh added.

The frictionless design of betting apps accelerates this cycle. Deposits are instant and one-click. Withdrawals require forms and waiting. Push notifications constantly nudge users toward the next bet. For a 24-year-old with a credit card and a phone, the distance between "fun side bet" and "serious financial trouble" can be measured in weeks.

The Bankruptcy Connection

The credit delinquency data is alarming on its own, but a separate study suggests the downstream consequences are even worse. Researchers at UCLA's Anderson School of Management, Harvard University, and USC's Marshall School of Business found that the odds of filing for bankruptcy increased by 10% to 25% in states with legal online sports betting. Average credit scores dipped, debt collection amounts rose by 8%, and increases in debt consolidation loans and auto loan delinquencies appeared roughly two years after legalization.

Poet Larson, a postdoctoral fellow at Harvard Business School's Digital Data Design Institute, described the weight of the evidence. "The various outcomes of delinquencies and credit scores [indicate] it seems to be leading to some harm among consumers," Larson told Fortune.

The $3 Billion Question

States collected nearly $3 billion in sports betting tax revenue during 2024. That sounds like a lot of money until you measure it against the costs. It amounts to a fraction of total state tax revenue, and it almost certainly doesn't cover the downstream economic damage: increased bankruptcies, debt collection, lost productivity, and the healthcare costs associated with gambling addiction.

The American Gaming Association has responded by launching a "responsible gaming" awareness initiative but opposes federal consumer protection regulations, arguing they would undermine state authority. That framing puts the burden on individual bettors to regulate themselves, which, given the app design and marketing machinery working against them, is a tall order.

Consider the math from the bettor's perspective:

- Average quarterly spend: $1,250 (and rising)

- House edge on most sports bets: 5% to 10%

- Annual expected loss for a regular bettor: $250 to $500+

- Credit card interest on gambling debts: 20% to 30% APR

Those numbers compound fast. A bettor who funds wagers with credit cards and chases losses can find themselves thousands of dollars in debt within a single football season. And unlike a bad stock pick, there's no underlying asset to recover. The money is simply gone.

The economic pressures already squeezing household budgets, from rising gas prices to elevated grocery costs, make this even more precarious. Families that might have absorbed a few hundred dollars in betting losses a decade ago now have far less margin for error.

What the Research Means Going Forward

This is the first time a Federal Reserve bank has published research directly linking legalized sports betting to deteriorating consumer credit at scale. That matters because the Fed's data and methodology carry institutional weight that academic studies alone may not. State legislatures considering further expansion of sports betting, or those debating whether to legalize it for the first time, now have a harder time arguing the activity is economically neutral.

The cross-border spillover effect is particularly significant. Even states that have chosen not to legalize betting are absorbing some of the financial damage as their residents place bets through apps when they travel to or live near legal states. That undercuts one of the core arguments for state-level regulation: that each state can independently manage its own betting ecosystem.

Several policy responses are on the table. Some researchers advocate for mandatory deposit limits, cooling-off periods between bets, and restrictions on credit card funding for gambling accounts. Others point to advertising restrictions, particularly during live sports broadcasts, as a way to reduce the constant pressure on vulnerable audiences. Australia and the UK have both moved toward stricter advertising rules for gambling companies, and early data suggests those measures can reduce participation among younger demographics.

But the political dynamics are tricky. States have built budgets around betting tax revenue. The sports industry itself is deeply intertwined with gambling companies through sponsorships, broadcast deals, and venue partnerships. Unwinding those relationships, or even restricting them, means fighting entrenched financial interests.

What Changes

The NY Fed study doesn't call for specific policy action. It presents data. But the data tells a clear story: legal sports betting generates real, measurable financial harm, especially for younger Americans. Credit delinquencies rise. Bankruptcies increase. Savings decline. And the effects don't stop at state borders.

For individual bettors, the takeaway is straightforward. Sports betting apps are designed to separate you from your money as efficiently as possible, and the evidence says they're very good at it. If you're betting on credit, you're compounding losses at 25% interest. If you're under 40, the statistics say you're more likely to end up in serious financial trouble than almost any other demographic.

For policymakers, the question is whether $3 billion in tax revenue is worth the credit destruction, bankruptcies, and addiction that come with it. The NY Fed just made that question a lot harder to dodge.